We often observe fast-growing SaaS companies finishing strong quarters, only to enter board meetings needing to explain why “GAAP revenue lagged behind bookings, again.” This situation arises not from poor sales performance, but rather because revenue recognition didn’t align with the structure of the deals.

Under ASC 606 and IFRS 15, revenue is recognized when the control of the promised service transfers to the customer. In the SaaS model, this typically means providing access over time, rather than a one-time delivery.

For subscription-based businesses, the timing and method of revenue recognition significantly impact various aspects such as board reporting, fundraising, and audit outcomes. This guide simplifies ASC 606 and IFRS 15 into easy-to-understand terms, featuring real-world SaaS examples that controllers and finance leaders encounter each quarter.

Understanding revenue recognition is crucial for establishing credibility.

Here’s the important point: many founders and even some CFOs may not realize until a controller brings it to their attention that SaaS revenue is not just about invoices; it’s centred around performance obligations.

That single principle can change everything.

A Quick Refresher: What ASC 606 and IFRS 15 Are Trying to Solve

At their core, these standards aim to answer one question: When has the customer actually received the value they paid for?

To answer that, ASC 606 introduced a principles-based five-step model, replacing industry-specific rules. But while simple in theory, each step is loaded with judgment, documentation, and system implications.

The Five-Step Revenue Recognition Model (With SaaS – Specific Insights)

1. Identify the Contract with a Customer

According to ASC 606-10-25-1, a contract exists only if the following conditions are met:

- Approval is obtained from both parties.

- The rights and payment terms are clearly stated.

- The contract possesses commercial substance.

- Collection of payment is probable (this aspect is often overlooked).

Controller Watchpoint: Early-stage SaaS companies frequently neglect proper collectibility assessments, especially when offering lenient terms to secure deals. Under ASC 606, revenue recognition cannot begin until collection is probable.

Additionally, contract modifications (such as upsells and extensions) may trigger reassessment as outlined in ASC 606-10-25-10 through 13. These modifications can create new contracts or alter the scope and pricing of existing ones; both scenarios are considered accounting events, not merely sales events.

2. Identify Performance Obligations

What exactly did we promise the customer? Common SaaS elements include:

- Software access (subscription)

- Implementation or onboarding

- Training

- Ongoing support or premium Service Level Agreements (SLAs)

Each of these could represent a distinct performance obligation under ASC 606-10-25-14. For example:

- Monthly platform access often consists of a series of distinct services that are recognized over time (ASC 606-10-25-14(b)).

- Implementation services may be treated as separate obligations and recognized either at a point in time or over time, depending on the level of customization and integration.

Controller Watchpoint: Many SaaS companies tend to under-segment their performance obligations, defaulting to straight-line revenue when parts of the contract should be separated.

3. Determine the Transaction Price

The transaction price is rarely limited to just the invoice amount. Controllers must evaluate:

- Variable consideration (ASC 606-10-32-6 to 14)

- Volume discounts

- Usage-based fees

- Credits and rebates

- Free trials

- Performance-based pricing

All of these elements must be estimated and constrained to avoid revenue overstatement and future reversals.

Additionally, significant financing components (ASC 606-10-32-15 to 20) should be considered:

- Annual prepayments are usually acceptable.

- Multi-year deals with deferred payments may require discounting for the time value of money.

- Consideration payable to customers (ASC 606-10-32-25) generally reduces revenue unless it is for a separate good or service.

4. Allocate the Transaction Price to Performance Obligations (SSP Is Key)

Use Standalone Selling Prices (SSPs) to allocate the transaction price (ASC 606-10-32-28). If observable prices do not exist:

- Utilize market assessment, cost-plus-margin, or residual methods.

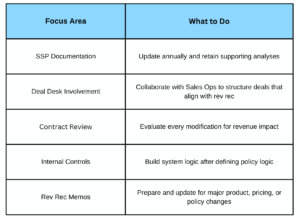

Controller Watchpoint: SSP assumptions are often scrutinized during audits, particularly when services are heavily discounted to win contracts. It’s essential to maintain documentation annually and align it with any changes in sales strategy.

5. Recognize Revenue When (or As) Performance Obligations Are Satisfied

Misalignment here distorts revenue trends, impacting everything from board dashboards to forecasting accuracy.

SaaS-Specific Revenue Scenarios Controllers Deal With Daily

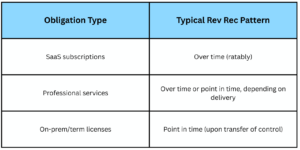

Subscription Revenue:

Recognized ratably over time, not when billed or cash is collected.

Professional Services: Often distinct performance obligations. Don’t automatically align their timing with subscription revenue. Free Trials and Discounts: Impact the transaction price, even when no cash changes hands.

Reseller Arrangements: Determine if the company is a principal or agent (ASC 606-10-55-36 to 40). This affects gross vs. net revenue reporting. Sales Commissions and Contract Costs:

- Under ASC 340-40, incremental costs to obtain a contract (e.g., sales commissions) are capitalized and amortized over the period of benefit.

- Practical expedient: If the amortization period is 1 year or less, you may expense immediately (ASC 340-40-25-4).

Controllers should revisit commission policies regularly, especially when renewals or variable comp structures are involved.

Implementation Challenges (and How Smart Controllers Navigate Them)

Systems and Data Fragmentation

Sales, billing, CRM, and accounting systems often don’t integrate well.

- Fix: Prioritize integration, not spreadsheets. Define clear system ownership between Finance and RevOps.

Internal Controls

Strong internal controls protect revenue integrity and support audit success.

- Fix: Automate revenue recognition only after establishing policy discipline and sign-off workflows.

Audit Readiness

Auditors want consistency, clear logic, and documentation. Not perfection.

- Fix: Maintain a revenue recognition memo library. Document key judgments for new products, pricing models, and deal types.

Team Training

ASC 606 is not “set and forget.” As your business evolves, so must your revenue recognition strategy.

- Fix: Invest in periodic training for accounting and sales ops teams. SaaS pricing evolves fast; your rev rec approach should too.

What This Really Means for SaaS Leadership

Revenue recognition is no longer a back-office task; it’s a strategic risk factor.

It affects:

- Board confidence and reporting accuracy

- Valuation models during fundraising

- Exit and audit readiness

- Investor credibility

Controllers who understand the business reality behind ASC 606, not just the technical rules, become strategic partners, not just compliance gatekeepers.

If you’re scaling, raising capital, or preparing for an audit or acquisition, getting this right early prevents painful reinstatements later.

Controller Quick Tips:

Contact our Dallas office for a complimentary CFO consultation to explore the benefits of Fractional Accounting with Bright Balance today!

![]()

![]()

![]()